Best character. The only correct answer is Omar. Best season. Season 4… although I have to say Season 3 had my favorite scene. Character I identify with. Photo finish but Kima Greggs wins (runner up is Stringer). See below.

@jae - I am seeing a small percentage of firms appoint MBA-qualified executives to lead their business direction (don’t ask me how many… I have no idea).

Are you observing more firms moving in the direction of having business people run their business?

Do you think that having business people run a law firm will lead to better outcomes for the law firm as a business?

What sorts of different behaviors can we expect from this type of law firm?

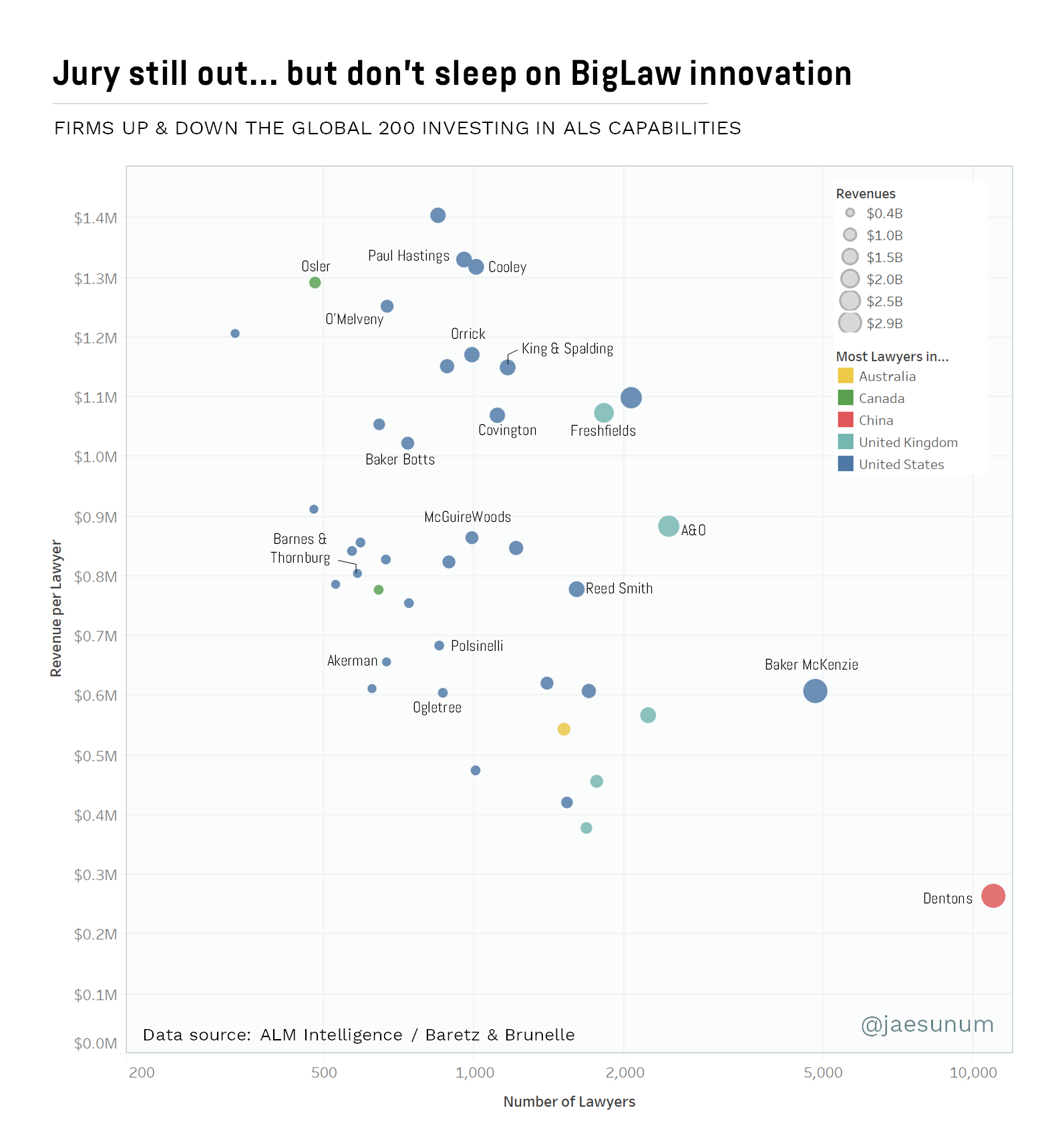

IT help desk is a no-brainer. It’s an already somewhat centralized back-office function, easy to centralize further into a service center, and the user journey is a fairly discrete and standardized end-to-end business process. Most importantly it doesn’t directly touch the revenue generating activities of the firm.

Not the case for Finance business processes or even conflicts, which you characterize as admin. Email, time entry, and turning time into bills are mission-critical business processes – downtime is not an option, so a straight lift-and-shift isn’t going to work.

Also keep in mind that there is process and tech debt in billing & new business intake processes. But spaghetti processes were put into place for a reason in the first place. Changing this wholesale without some traceability as to why current workarounds are needed is a high-risk endeavor.

Kima Greggs is a great avatar for anyone who operates in a space where people do not understand the value you bring because they are not fluent in your skill set.

I have not operated in the business tier of a law firm, but when I consumed these services as a practicing attorney I observed they were spread across many delivering teams. If still true, I suspect finding convergence, synergies, and economies of scale will be hard because of the fractured incentives and coordination costs.

Defense against mounting pressure, depending on current position (client + service mix). Some firms were early in this effort because they are heavily invested in areas that were price-pressured, being disaggregated by clients / displaced by vendors. e-Disc is an easy example, but IP (trademarks) and L&E (single-plaintiff claims, routine benefits) are other examples.

Organizational resourcing / capacity for scale. Large globals / international firms with scale are a good example. These firms have the opportunity to serve clients across a broader band in the value spectrum, and could invest in fuller models to “future proof” and defend a bigger swath of legal demand.

By fuller models, I mean beyond straight labor arbitrage, greater process discipline + tech enablement.

It’s probably instructive to note this is very hard. Lots of firms experimented with JUST labor / wage arbitrage (think this will continue due to need for more diverse career pathways off the partner track). BUT it’s relatively new for law firms to engage in business model innovation. I was lucky to learn from Josh Kubicki and Rob Saccone at Seyfarth while we assessed the firm’s strategic position and the need to build capabilities in service design + change management. It’s really really really hard.

Some firms don’t do it because they don’t have a clear strategic reason to. Others try and fail because it’s really hard. Still, captive ALS is an important trend to watch.

I agree on both #1 (defensive) and #2 (opportunity because of scale).

And the labor arbitrage point is key. Some early outsourcing was only about this (get me lawyers in India at $22/hour instead of $55 in NYC). The smart clients, early and still, work with providers to redesign the process and deploy more tech.

I sometime worry, however, about transforming the business model. I see the need but if law firms think they must do that, fewer will reduce their cost basis. That is, I think captive ALSPs can co-exist in the existing business models.

“IT help desk is a no-brainer” - I think if you reconceptualize the help desk as a “lawyer / staff success center” you can turn it into (1) a cost into an investment; with (2) its operations becoming “outbound” during low demand periods.

This will be particularly important as the pace of tech change accelerates.

SO. I would not use this phrasing. Instead I would say

Clients need to (and by all accounts want to) rationalize their supply chain. The biggest buyers who buy globally at scale have a legal supply chain of over 500+ (in some cases 1000+) providers.

Firms need to (but aren’t equipped or used to) rationalize their client roster. The 30 or so biggest firms in the world probably have client rosters between 5,000 and 20,000 clients.

Firing / deselection are abrupt events. Especially in the enterprise law market, abrupt events are bad: for clients it means disruption to business continuity and often erosion of overall customer experience for the END-user of services (often “the business.”) For law firms, abrupt terminal events to client relationships are bad: they hurt the responsible partners and they hurt all fee earners dependent on the relationship, not only for this year’s hours / billables, but in depth of relationship / access to opportunities.

In order to plan & execute the necessary rationalization, deeper understanding is required on both sides that raise hard questions. Some of these questions are very much the questions that need asking and answering.

For clients the questions might be: Where and why are we experiencing expanding demand? Which are our MOST important tranches of demand? How might we optimally get that work done (the right people, the right models, the right tooling)? Which of our current supplies have (and are able to leverage) truly valuable institutional knowledge?

For firms the questions should be: Which are our MOST important clients? What do they buy from us now and where are we best positioned to serve them in future? Where should we compete (practice/industry, not just geography)? Where are we most advantaged? Which areas are distractions for us?

Why do these questions not get answered? Because they’re super hard. So we use heuristics and proxies (e.g. both clients and firms prioritize stakeholders who complain the loudest; firms conflate biggest clients – e.g. highest billings this year or last year – with most important). We substitute easier questions for the hard ones. This is bad because it leads us down the wrong path.

One concrete reason is because the current data environment and the legacy BI/reporting infrastructure don’t support the exploration of these questions. In fact, we also have spaghetti code / accumulating process + technical debt that sometimes active IMPEDE smart thinking about these questions. (Shameless plug: THIS IS WHY I AM SO EXCITED ABOUT DATANA. We are going to work on these issues. I promise!)

Basically, this is bad and I don’t recommend it bc it further impedes psychological safety on all fronts:

I do support more intentional and deliberate strategic matching across the buy-side and supply-side. This will take work and time, and likely investment in strategic client-firm relationships as well as more advanced analytics tooling.

A dichotomy? Law firms are often selling a credence good. As they start moving into ALSP style work they bring more process and measurement to the work. This can establish more objective measures of value. Does this change client expectations for more conventional firm work too? Once you know something can be measured for speed, quality, and cost, can you go back to not knowing?

So we should be investing in measurement systems that help us understand demand and supply characteristics for work so we create more accurate matching AND prediction functions? Makes sense to me.

For shorthand purposes / a bit of preface… I am going to refer to three distinct but related aspects/prerequisites of what you describe here:

Platformization: (a) tech platforms that allow building on top and (b) two-sided platform business models

Democratization via (a) more diverse/accessible “builder” / “creator” tools (e.g. no code, low-code); (b) open source development as you mention

Openness via improved flow of information, data, knowledge & insight across organizational boundaries. Interoperability is key here from a technical standpoint but there’s also ethos involved. Some organizations demonstrate a STRONG preference to build rather than partner (this applies outside of legal. For instance FB builds their own data centers – in fact the data center build-out is a key capability + competitive advantage for them.) Apple has interesting ethos that has evolved over time in terms of nearly religious belief in closed system from a technical standpoint but instead creating marketplace/platform dynamics in GTM/biz model.

Soooo… this is such an excellent line of questioning. To play apologist for a second… there is a long history of ethos against openness in legal and a propensity to prioritize control and security. This has roots in very valid reasons.

Bearing in mind what I said with respect to supply chains / client rosters:

So this has a lot of non-obvious implications. Basically the balkanization in our industry is fractal and has MANY substrates. Legal is also a market that is ruled by power curves (top heavy + long tails everywhere). Just like it is difficult to rationalize commercial principles that govern how we transact #legalbiz, it is really, really, really hard to make policy on how we manage #legaltech and most importantly each organization’s #data and #knowledge assets, with SO many stakeholders in each micro-ecosystem where most will have this propensity for control + security over openness (e.g. 1 buyer + many suppliers OR 1 supplier + many, many buyers).

So yes, we have mounting complexity and worsening balkanization. This is bad, for everyone. But it is a wicked problem in that individual players making defensible/rational decisions to pursue the local maxima or avoid the local minima results in severe suboptimality in the ecosystem.

( plug here for Reynen Court. Hi @clang!) One really, really, really important function that RC aims to fill is to create a standardization / market-making layer for infrastructure, with emphasis on security assurance. THis is important not only for the direct benefits in the proffered value proposition but ALSO for the gradual shift in ethos for the industry: we have to meet firms and clients where THEY are in their journey and work WITH them to increase their level of overall comfort with new and varied approaches to old and intractable problems. RC is not the WHOLE solution to what you’re asking about but I fully believe that RC will mosdef, for sure drive progress in areas where new approaches and new intermediaries are SORELY needed.

In terms of the radical reduction in cost and time-to-market enabled by very open environments filled with cloud-native app development… we are probably a ways off from that in legal. However, we do have expanding and broadening #appdev toolbox and tech platforms (although with varying degrees of openness) that provide a better set of “builder/maker” tools. So I think there is already progress and we will continue to see more.

So… have hope? “True digital transformation” in ANY vertical is a long-haul effort. Also, everyone is grappling with this now. Seriously. BCG and McKinsey write about this all the time. BCG says 70% of digital transformations fall short of objectives. So we can definitely do better in legal… but what you’re talking about is really paradigm-shifting, world-changing stuff. It is super difficult so we have to keep at it.

It may be a little bit more complicated: we need to (1) look for weak signals of emerging phenomenon (in demand or supply); (2) develop agility to shift legal operations to met those uncertain changes; while also (3) understanding current “standardized” demand; and (4) optimizing to supply those needs. The first two - 1 and 2 - are about exploring in conditions of uncertainty / complexity; and second two - 3 and 4 - are about exploiting with (mostly) known bounds.

Great point on legal services being credence goods. But the same can be said for quasi-legal services and really anything that carries risk. For instance, you can outsource patent searches (non-legal work) until a prior art reference is missed (creating legal risk). Only way you can measure effectiveness is post-facto (comparing litigated patents in a service done in-house vs one that employed an ALSP search team). This data is hard tom come by even for non-legal /quasi-legal services. So, you are only measuring cost and throughput. Quality is really only a proxy based on who ever is qualifying the output (e.g., client or supervisor). All this to say, that the measures of value tend to be cost -related until proven otherwise. This makes it really hard to shift the conversation away from cost.

@chgamez you gave us the answer. Start connecting work inputs and characteristics to outcomes. With respect to quality, if we can collective identify the traits and features of work with higher quality, we can remove some of the bias that does not serve us.

James! Thanks for this very thoughtful and super, super, super important question.

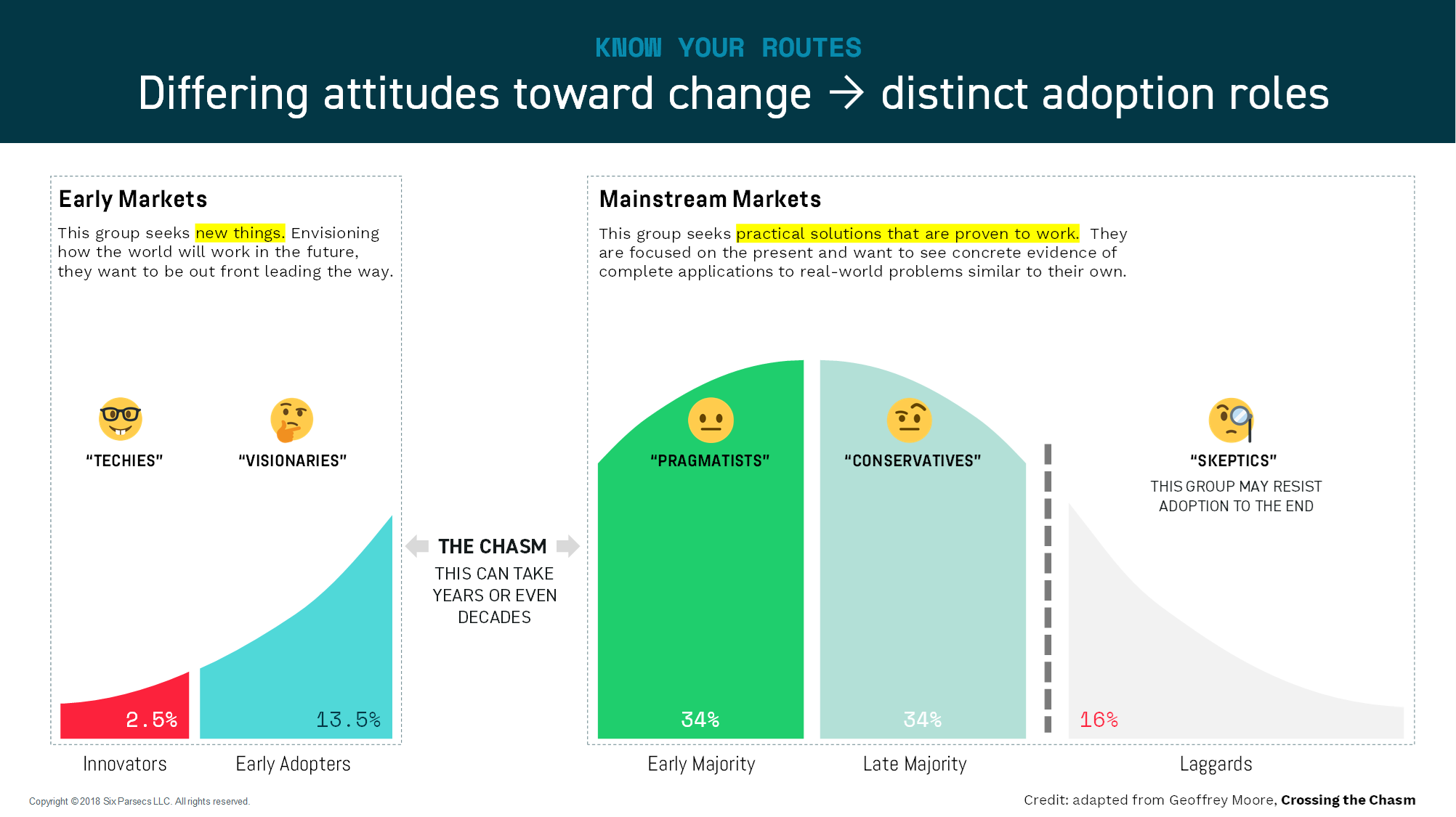

I think I need to clarify what I meant by “core” vs “frontier” tech, but before I get into that I would point people to the tireless work that Bill Henderson has done on the Legal Evolution publication (apart and aside from my own contributions) around diffusion theory. His foundational posts (007) and 008 are really aimed at reconciling the lived experiences of individuals ( everything so slow and painful, hype cycles, etc.) with the gradual but ongoing progress of the overall system. I added some color on how to apply this theory to #legaltech sales here.

So for the purposes of today’s, I’ll just reference the graphic below

Essentially, what I meant by “core” tech is stuff that has been tested/used enough to be established as a good/better way to work and reliable enough to perform with acceptable execution risk. What I meant by “frontier” tech is application of component tech into products that either haven’t found product-market fit or haven’t been tested sufficiently in the wild.

Going back to the very good points/questions you raise… I do think we see in legal lots of “core tech” that ought to be mainstream by now but aren’t. They fall into the chasm. (This also happens outside of legal… or https://www.amazon.com/dp/B000FC119W/ref=dp-kindle-redirect?_encoding=UTF8&btkr=1 wouldn’t be such a popular tech marketing book).

SHOULD legal tech cos be considering a services model? Yes, I think so, with some qualifications and disclaimers.

Firstly, I’m not sure that everything we bill as “legal tech” is actually software. Sometimes it is just process/workflow glue, which is heavily context-dependent and requires services to be wrapped around the tech components. At the other end of the spectrum, we also have “appdev toolbox” platform offerings that require either an advanced/skilled user base OR a strong services component for enablement (way beyond customer success or pre-deployment configuration).

It’s important to flag that service and tech businesses have VERY different multiples that should inform VERY different strategic approaches to funding, GTM and growth. I would think that the higher SaaS multiples will deter founders from considering the services component. That’s cold hard reality but I still think they need to think about what services needs customers will experience around the tech and solve for that, whether it’s true the core offering, value-add services, add-on services, or through partnership.

That said, I don’t want to discourage or dissuade current or would-be founders from building tech. I just think (and I think you’d agree from your question) that the business model requires a lot of flexible/creative thinking about how a new startup/new tech will actually integrate with existing/emerging components in the market ecosystem. Because we only make progress in the system when that exploration does hit on game-changing tech, either wrapped / supported / complemented by changes to the services environment around it, tip rates of adoption from the early markets to the mainstream markets.

Meandering answer but definitely important Qs to raise and lots of room to ponder/explore/discuss further.

Excellent question, and one I’ve discussed with many different players in the legal ecosystem. To paraphrase and pose to @jae (and please correct me if I misunderstood the original Q), if law firms are unwilling or unable to utilize new tech/svc offerings that actually demonstrate downstream value to legal service buyers, should the providers of said tech/svcs consider competing instead of partnering?

IMO - this has happened before and will happen again, increasingly. See contract tech, for example. whether you call them ASLPs or not.

Agree. The easiest way to do this is to change desired value outcomes. So for example, when drafting a contract the desired value is (client: I want full coverage) – hard to measure ex-ante. However if client says: I want this to be shorter, readable and visual – then there is a non-cost related value that can be assessed. Shameless plug for Frontline Managed Services (my new employer) – when the billing service provider can say I can take your realization rate from 85% to 94%, then does it, the outsourcing conversation is totally about value and not cost (e.g., doesn’t matter if it’s cheaper). Until a managed service provider can clearly articulate a value detached from a cost kpi, it’s all a cost-reduction conversation (not always the most compelling).

Best character. The only correct answer is Omar.

Best character. The only correct answer is Omar. Best season. Season 4… although I have to say Season 3 had my favorite scene.

Best season. Season 4… although I have to say Season 3 had my favorite scene. Character I identify with. Photo finish but Kima Greggs wins (runner up is Stringer). See below.

Character I identify with. Photo finish but Kima Greggs wins (runner up is Stringer). See below.

Carlos! … plus entire Frontline team

Carlos! … plus entire Frontline team  )

) I don’t see this as a no-brainer. I support this type of cost innovation but there are significant barriers depending on business context, stakeholder groups, etc. The key is to understand how each of these efforts might fit into (a) the overall prioritization across each firm’s unique portfolio of transformation initiatives; (b) change management lift of each endeavor, which goes directly to the stakeholders whose behaviors, work context and behaviors/habits need some shifting; © opportunity cost of such efforts.

I don’t see this as a no-brainer. I support this type of cost innovation but there are significant barriers depending on business context, stakeholder groups, etc. The key is to understand how each of these efforts might fit into (a) the overall prioritization across each firm’s unique portfolio of transformation initiatives; (b) change management lift of each endeavor, which goes directly to the stakeholders whose behaviors, work context and behaviors/habits need some shifting; © opportunity cost of such efforts. IT help desk is a no-brainer. It’s an already somewhat centralized back-office function, easy to centralize further into a service center, and the user journey is a fairly discrete and standardized end-to-end business process. Most importantly it doesn’t directly touch the revenue generating activities of the firm.

IT help desk is a no-brainer. It’s an already somewhat centralized back-office function, easy to centralize further into a service center, and the user journey is a fairly discrete and standardized end-to-end business process. Most importantly it doesn’t directly touch the revenue generating activities of the firm. Not the case for Finance business processes or even conflicts, which you characterize as admin. Email, time entry, and turning time into bills are mission-critical business processes – downtime is not an option, so a straight lift-and-shift isn’t going to work.

Not the case for Finance business processes or even conflicts, which you characterize as admin. Email, time entry, and turning time into bills are mission-critical business processes – downtime is not an option, so a straight lift-and-shift isn’t going to work. Also keep in mind that there is process and tech debt in billing & new business intake processes. But spaghetti processes were put into place for a reason in the first place. Changing this wholesale without some traceability as to why current workarounds are needed is a high-risk endeavor.

Also keep in mind that there is process and tech debt in billing & new business intake processes. But spaghetti processes were put into place for a reason in the first place. Changing this wholesale without some traceability as to why current workarounds are needed is a high-risk endeavor.

I’ll answer on the air… (

I’ll answer on the air… ( Basically, this is bad and I don’t recommend it bc it further impedes psychological safety on all fronts:

Basically, this is bad and I don’t recommend it bc it further impedes psychological safety on all fronts:

I do support more intentional and deliberate strategic matching across the buy-side and supply-side. This will take work and time, and likely investment in strategic client-firm relationships as well as more advanced analytics tooling.

I do support more intentional and deliberate strategic matching across the buy-side and supply-side. This will take work and time, and likely investment in strategic client-firm relationships as well as more advanced analytics tooling.

Thank youuuu!

Thank youuuu!

Bearing in mind what I said with respect to supply chains / client rosters:

Bearing in mind what I said with respect to supply chains / client rosters: really, really, really hard

really, really, really hard  to make policy on how we manage

to make policy on how we manage  So yes, we have mounting complexity and worsening balkanization. This is bad, for everyone. But it is a

So yes, we have mounting complexity and worsening balkanization. This is bad, for everyone. But it is a  plug here for Reynen Court.

plug here for Reynen Court.  So… have hope? “True digital transformation” in ANY vertical is a long-haul effort. Also, everyone is grappling with this now. Seriously.

So… have hope? “True digital transformation” in ANY vertical is a long-haul effort. Also, everyone is grappling with this now. Seriously.  hype cycles, etc.) with the gradual but ongoing progress of the overall system. I added some color on how to apply this theory to

hype cycles, etc.) with the gradual but ongoing progress of the overall system. I added some color on how to apply this theory to  So for the purposes of today’s, I’ll just reference the graphic below

So for the purposes of today’s, I’ll just reference the graphic below

SHOULD legal tech cos be considering a services model? Yes, I think so, with some qualifications and disclaimers.

SHOULD legal tech cos be considering a services model? Yes, I think so, with some qualifications and disclaimers. Firstly, I’m not sure that everything we bill as “legal tech” is actually software. Sometimes it is just process/workflow glue, which is heavily context-dependent and requires services to be wrapped around the tech components. At the other end of the spectrum, we also have “appdev toolbox” platform offerings that require either an advanced/skilled user base OR a strong services component for enablement (way beyond customer success or pre-deployment configuration).

Firstly, I’m not sure that everything we bill as “legal tech” is actually software. Sometimes it is just process/workflow glue, which is heavily context-dependent and requires services to be wrapped around the tech components. At the other end of the spectrum, we also have “appdev toolbox” platform offerings that require either an advanced/skilled user base OR a strong services component for enablement (way beyond customer success or pre-deployment configuration). It’s important to flag that service and tech businesses have VERY different multiples that should inform VERY different strategic approaches to funding, GTM and growth. I would think that the higher SaaS multiples will deter founders from considering the services component. That’s cold hard reality but I still think they need to think about what services needs customers will experience around the tech and solve for that, whether it’s true the core offering, value-add services, add-on services, or through partnership.

It’s important to flag that service and tech businesses have VERY different multiples that should inform VERY different strategic approaches to funding, GTM and growth. I would think that the higher SaaS multiples will deter founders from considering the services component. That’s cold hard reality but I still think they need to think about what services needs customers will experience around the tech and solve for that, whether it’s true the core offering, value-add services, add-on services, or through partnership. That said, I don’t want to discourage or dissuade current or would-be founders from building tech. I just think (and I think you’d agree from your question) that the business model requires a lot of flexible/creative thinking about how a new startup/new tech will actually integrate with existing/emerging components in the market ecosystem. Because we only make progress in the system when that exploration does hit on game-changing tech, either wrapped / supported / complemented by changes to the services environment around it, tip rates of adoption from the early markets to the mainstream markets.

That said, I don’t want to discourage or dissuade current or would-be founders from building tech. I just think (and I think you’d agree from your question) that the business model requires a lot of flexible/creative thinking about how a new startup/new tech will actually integrate with existing/emerging components in the market ecosystem. Because we only make progress in the system when that exploration does hit on game-changing tech, either wrapped / supported / complemented by changes to the services environment around it, tip rates of adoption from the early markets to the mainstream markets.